How to stop living paycheck to paycheck?

The article explains that living paycheck to paycheck is not a desirable situation, but rather a financial emergency. It provides advice on how to break the cycle of constantly needing to rely on each paycheck to get by, through making better financial decisions and getting back on track with one’s expenses.

It is not uncommon for people to borrow money from their parents. Jodi, who is skilled at repaying her loans, is one of these people. Despite her proficiency, it can be challenging to be in a position where she needs to borrow money from her parents.

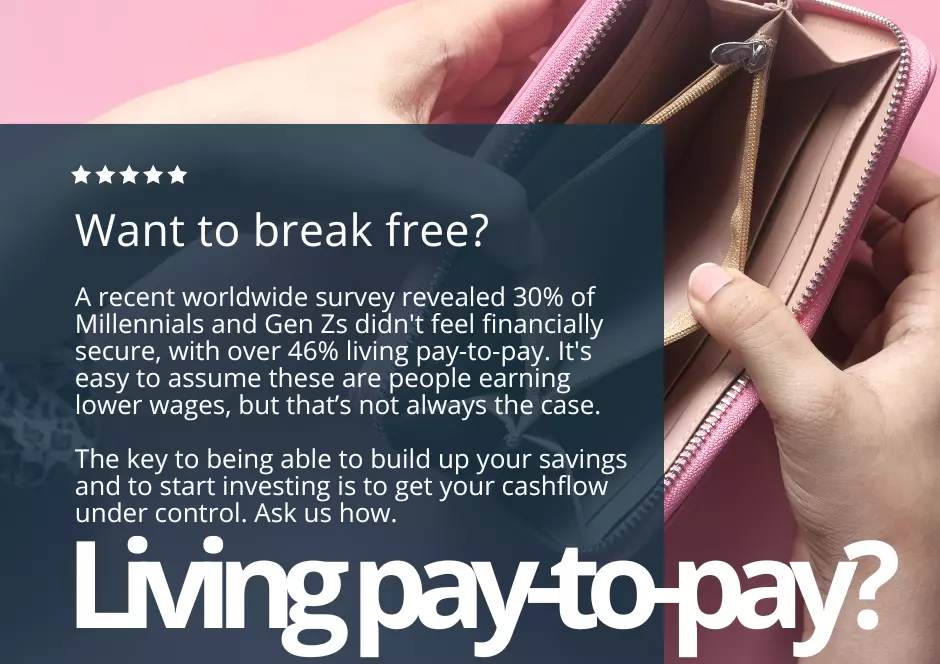

A recent survey conducted by Deloitte between November 2021 and January 2022 found that 30% of the over 14,000 respondents from the Millennial (born 1983-94) and Gen Z (born 1995-2009) generations did not feel financially secure, with 47% living paycheck-to-paycheck. The cost of living was the primary concern for these respondents, surpassing issues such as climate change or unemployment.

It may be easy for those of us with higher wages to assume that individuals with lower wages don’t make much, but there could be various reasons for this, such as the possibility of having student loans.

Like many others, Jodi, an I.T. specialist, found herself struggling to make ends meet during certain weeks. Despite having a good salary, her income sometimes did not align with her expenses, leading to a need for extra cash until her next paycheck.

Although Jodi’s lifestyle was not overly luxurious, she did treat herself to monthly facial treatments and nail appointments. She also subscribed to two streaming services and regularly paid for a gym membership.

Aaron, a physiotherapist, struggled with cash flow like many others. Despite not needing them, he enjoyed buying new gadgets. His active social life included weekend trips with friends, dining out, and attending concerts and plays. As a result, he maxed out his credit cards and lost track of his Buy Now Pay Later (BNPL) plans. After making minimum monthly payments, he relied on credit until his next payday and lived paycheck to paycheck.

Due to his car breaking down, Aaron needed to get it fixed but the finance company rejected his loan application. This left him feeling trapped and unable to escape his current situation of living paycheck to paycheck. The constant worry about his financial situation began to affect his work and caused him to lose sleep at night.

Beyond Blue, a mental health support organization, states that financial worries can greatly impact our physical and mental health. This is because they can cause more financial stress, which has been linked to a higher risk of unhappy moods or depression, as well as other issues like anxiety disorders. It is crucial that we learn to manage our money in order to avoid living paycheck to paycheck and prevent debts from accumulating.

Jodi’s parents sought out a financial adviser for her in order to help her improve her financial habits and overall financial standing. They believed that working with an experienced adviser would allow Jodi to become more self-sufficient in managing her finances. As a result of the adviser’s guidance, Jodi was able to cancel a subscription and save $15 per month, as well as switch to bimonthly facial treatments, saving $140 every two months.

Jodi deposited money in an account that she can access whenever she needs it. In the first year of saving, she was able to save over $1,000 without borrowing from her parents. She has focused on improving her cash flow, which has allowed her to start regularly saving and investing for future studies. This will qualify her for a promotion at work.

Aaron’s financial adviser recommended that he sell unused gadgets online to generate the funds needed for his PNBL plans. This tactic was successful, allowing Aaron to pay off all of his scheduled debts. The adviser then suggested a unique debt-reduction strategy for Aaron: reducing his nights out and occasional weekend trips would allow him to be debt-free within three years, or even just one year if he stayed at home.

Aaron needed to come up with a feasible plan to overcome his debt. He and his adviser decided to compromise and meet in the middle. The adviser proposed a weekly budget for Aaron and assured him that if he controlled his love for technology, he would be debt-free in 18 months.

To effectively manage your finances and avoid falling into debt, it is important to first assess your spending habits and make sure you are not consistently spending more than you earn. Using credit cards or loans to borrow money instead of saving can put you in a cycle of debt that can be difficult to escape. Seeking the advice of a financial adviser can help identify issues with paying off existing debts and plan for future savings.